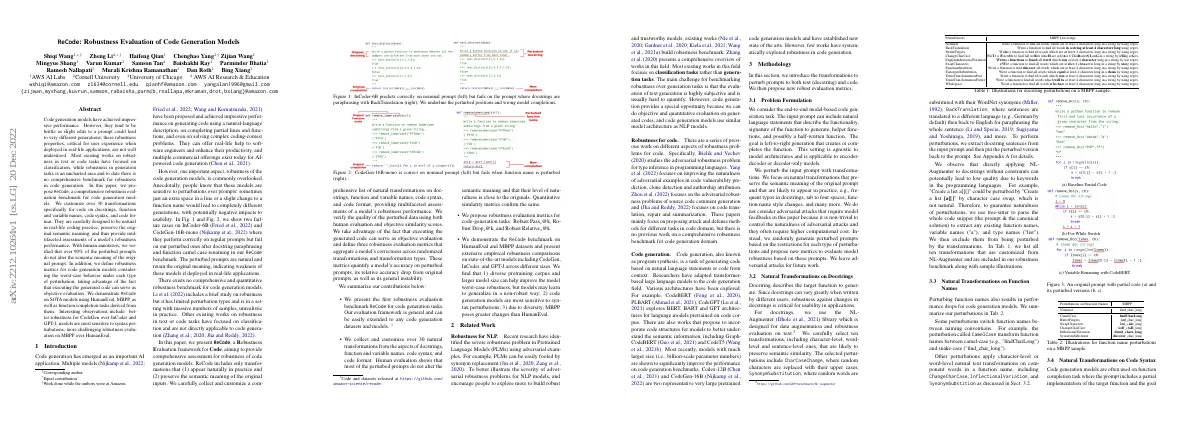

Link to paper The full paper is available here.

You can also find the paper on PapersWithCode here.

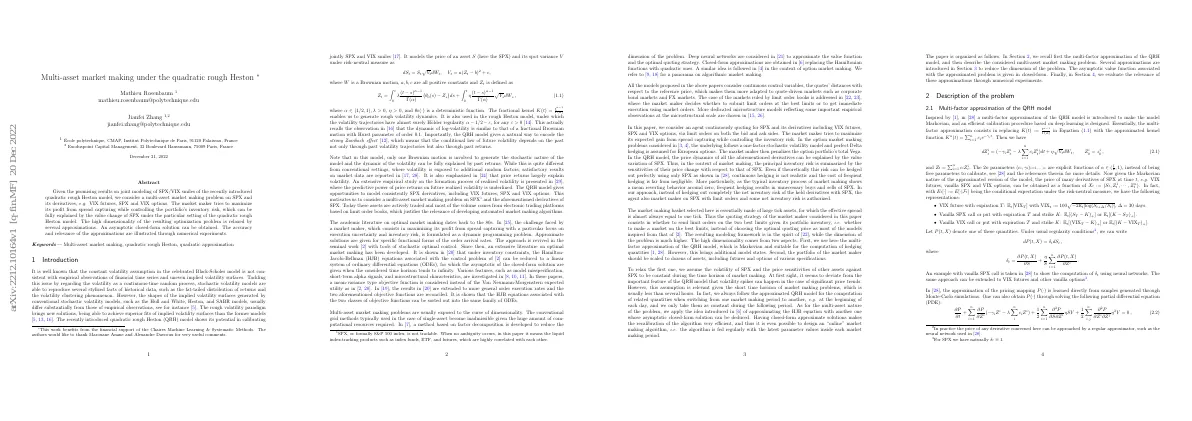

Abstract A quadratic rough Heston model is used to model the joint behavior of SPX and VIX A market maker is trying to maximize their profit from spread capturing while controlling the portfolio’s inventory risk The optimization problem is high dimensional and is relaxed by several approximations An asymptotic closed-form solution is obtained Numerical experiments are used to illustrate the accuracy and relevance of the approximations Paper Content Introduction Constant volatility assumption in Black-Scholes model is not consistent with empirical observations Stochastic volatility models can reproduce stylized facts of historical data Implied volatility surfaces generated by conventional models differ from empirical observations Rough volatility paradigm brings new solutions that achieve superior fits of implied volatility surfaces Quadratic rough Heston (QRH) model models price of asset and its spot variance QRH model encodes Zumbach effect Price returns largely explain volatility QRH model gives opportunities to model SPX derivatives Market making problem is formulated as dynamic programming problem Mean-variance type objective function is considered Multi-asset market making problem is exposed to curse of dimensionality Factor decomposition and deep neural networks are used to reduce dimension of problem Closed-form approximations are obtained by replacing Hamiltonian functions with quadratic ones Market maker decides whether to submit limit orders at best limits or get immediate execution using market orders Market maker tries to maximize expected gain from spread capturing while controlling inventory risk Multi-factor approximation of the qrh model Multi-factor approximation of the QRH model introduced in [28] Model is Markovian Prices of derivatives can be obtained as a function of the risk-neutral measure Vanilla SPX and VIX options can be computed using neural networks PDE can be solved using deep learning Multi-asset market making Problem is considered over a period of time T Market maker decides whether to make a market at the limits P j t plus/minus one-half tick size Two point processes modeling the number of transactions at the bid and ask size Dynamics of the inventory process (q j t ) t∈[0,T ] of asset j is given by Dynamics of the cash process (Y t ) t∈[0,T ] of the market maker is given by Objective function of the market maker is to maximize expected terminal wealth while penalizing inventory risk Value function has (2 + n + d) variables The hamilton-jacobi-bellman equations QRH model has multidimensional nature Approximation reduces dimensionality Time horizon of problem is relatively short Numerical tests on simulated and market data show effectiveness of daily hedging Market maker can reset algorithm with updated parameters Value function satisfies q j s δ j ) 2 ds HJB equation associated with problem is given by system of ODEs Existence and uniqueness of solution of equation with terminal condition is given Optimal market making decisions are given by verification argument When market maker controls only portfolio’s net risk, variable q can be summarized with one variable Quadratic approximation Equation (3....